The DPDP Act for BFSI sector arrives at a time when Indian banks and financial institutions are already rethinking how they use data. Over the years, customer information was collected carefully but generously. Forms were detailed, records were thorough and much of this data lived quietly in branch files and storage rooms.

Things look very different today.

Banks are digitising records, building centralised data platforms and using AI to improve decisions, speed and customer experience. This brings legacy data into focus. It also gives BFSI leaders a clear moment to pause, review and design data practices that are simpler, cleaner and more transparent for customers.

Why the DPDP Act feels personal for BFSI leaders

Few sectors understand responsibility quite like BFSI. Banks and insurers already operate under multiple regulatory frameworks and handle deeply sensitive information.

The DPDP Act builds on this foundation. It formally defines banks as Data Fiduciaries, placing them in charge of ensuring personal data is collected and used only for clear, lawful purposes.

Rather than introducing something entirely new, the Act encourages discipline. It asks a simple question: Why are we collecting this data, and how long do we really need it?

For many BFSI organisations, answering this question is the first step towards stronger governance and better data quality.

Rethinking how much customer data is really needed

Traditionally, data collection in banking leaned towards being comprehensive. It helped future-proof processes and supported multiple downstream uses.

Under the DPDP Act, the focus shifts to data minimisation. This does not mean collecting less data blindly. It means collecting relevant data with intent. Regulators have already encouraged banks to revisit onboarding and servicing processes. The goal is not restriction, but clarity.

In practice, this involves:

- Clearly explaining why specific data is needed.

- Collecting consent in a way customers can understand.

- Letting go of data once its purpose is complete, unless laws require retention.

- Protecting data through strong but practical safeguards.

Many BFSI teams find that this exercise simplifies operations rather than complicating them.

How BFSI organisations are responding in practice

Across the sector, DPDP readiness is driving thoughtful internal change.

Some banks have created dedicated data privacy offices, led by Data Privacy Officers (DPO) who work closely with IT, security, legal and business teams. This helps privacy decisions stay connected to real operations.

We are also seeing a steady move towards:

- Enterprise-wide data mapping to understand where data lives

- Clear articulation of lawful purposes for data use

- Consent management tools that integrate with existing systems

- Targeted training so teams understand privacy in their daily roles

The phased rollout of the DPDP framework gives organisations time to build these foundations properly. Early focus is on visibility and alignment. Later stages will naturally mature into automation and audit readiness.

Navigating reporting and retention with confidence

One area that often raises questions is breach reporting. BFSI organisations may need to coordinate notifications across sectoral regulators and the Indian Computer Emergency Response Team (CERT-In). With the right playbooks and communication workflows, this becomes a manageable process rather than a stressful one.

Another practical consideration is balancing customer deletion requests with legal retention obligations under frameworks such as PMLA and RBI guidelines. Many banks are adopting conditional erasure approaches. These separate mandatory records from optional data, making it easier to respect customer rights while meeting statutory requirements.

This clarity reduces confusion for both customers and internal teams.

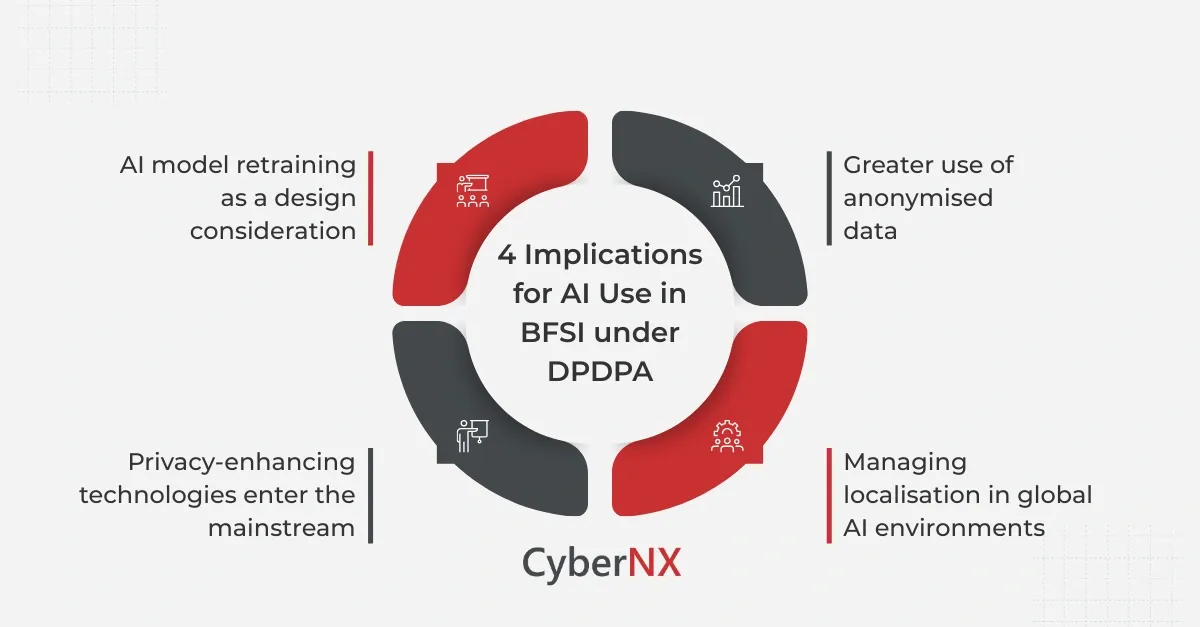

What the DPDP Act means for AI in BFSI

AI continues to play a growing role in fraud detection, credit assessment, service automation and risk management. The DPDP Act does not slow this progress. Instead, it brings structure.

AI systems now need to align more closely with consent and purpose definitions. This encourages better data hygiene and more intentional model design.

1. AI model retraining as a design consideration

When customers withdraw consent or request erasure, some AI models may need updates. Planning for this early helps teams avoid disruption later. This is leading BFSI organisations to think about modular, adaptable AI pipelines rather than static models.

2. Greater use of anonymised data

Anonymisation supports both privacy and scale. Many AI teams are refining techniques to maintain accuracy while reducing reliance on identifiable data. This approach often improves model robustness.

3. Managing localisation in global AI environments

For banks using global AI platforms, data localisation requirements encourage clearer data boundaries and stronger vendor governance. Over time, this improves transparency across the ecosystem.

4. Privacy-enhancing technologies enter the mainstream

Technologies like federated learning and differential privacy are becoming practical tools rather than theoretical ideas. They allow insights without exposing raw data. From what we see, BFSI teams that explore this early gain long-term flexibility.

Privacy becomes part of data architecture

One of the most positive shifts driven by the DPDP Act is architectural.

Instead of large, open-ended data lakes, organisations are creating purpose-bound data zones. Each dataset has a clear use case, consent reference and retention rule.

Customer journeys are also improving. Consent is becoming clearer, easier to manage and simpler to withdraw. This architectural clarity supports compliance while making analytics and AI more reliable.

Governance expectations for larger BFSI institutions

Large banks are likely to be designated as Significant Data Fiduciaries. This brings additional governance expectations, including impact assessments, audits and algorithm oversight.

Rather than being a burden, these measures help institutionalise good practices. Governance moves from manual tracking to embedded workflows that scale. AI teams benefit from clearer documentation, better accountability and smoother regulatory conversations.

Many BFSI leaders view the DPDP Act as a chance to strengthen customer relationships. When customers understand how their data is used and feel in control, trust grows naturally. Over time, this trust supports digital adoption, engagement and loyalty. Privacy becomes part of the brand experience, not just a compliance checkbox.

Conclusion

The DPDP Act in BFSI offers a timely opportunity to simplify data practices, strengthen AI foundations and build trust through transparency.

Organisations that treat privacy as a design principle rather than a late-stage fix will find it easier to innovate responsibly. The result is AI that is effective, compliant and aligned with customer expectations.

At CyberNX, we help BFSI teams translate DPDP requirements into practical data security and AI governance frameworks. Our experience shows that thoughtful changes today create smoother operations tomorrow. If you are reviewing your DPDP and AI readiness, our DPDPA Consultation experts will be happy to support that journey.

DPDPA, BFSI and AI Readiness FAQs

Does the DPDP Act require banks to stop using AI?

No. It encourages AI that is built on clear consent, purpose limitation and strong governance.

How should banks handle old customer records under DPDP?

Once digitised for analytics or AI, legacy records should be mapped, classified and governed like any other digital personal data.

Are customers likely to engage more with privacy controls?

Yes. Clear and simple consent options often increase customer confidence and participation.

Is DPDP compliance mainly a legal exercise?

Not really. It is equally about data architecture, process design and technology alignment.